All Categories

Featured

Table of Contents

- – Why is What Is Level Term Life Insurance? impo...

- – What should I know before getting Level Term L...

- – What is a simple explanation of Level Term Li...

- – Is Level Term Life Insurance Protection worth...

- – What is the difference between Level Term Li...

- – Level Term Life Insurance For Young Adults

Costs are generally lower than whole life plans. With a level term policy, you can select your insurance coverage amount and the policy size.

And you can't squander your plan throughout its term, so you won't obtain any financial benefit from your previous coverage. Just like other types of life insurance policy, the expense of a degree term plan relies on your age, coverage needs, work, lifestyle and wellness. Generally, you'll discover extra cost effective protection if you're younger, healthier and much less dangerous to insure.

Since degree term costs remain the very same throughout of protection, you'll recognize exactly just how much you'll pay each time. That can be a huge aid when budgeting your expenditures. Degree term coverage additionally has some adaptability, allowing you to personalize your policy with added features. These often can be found in the form of bikers.

You might have to fulfill particular problems and certifications for your insurance firm to establish this biker. On top of that, there might be a waiting duration of as much as six months prior to working. There additionally might be an age or time limitation on the protection. You can add a kid biker to your life insurance policy plan so it also covers your children.

Why is What Is Level Term Life Insurance? important?

The survivor benefit is usually smaller sized, and coverage normally lasts until your youngster turns 18 or 25. This rider might be a more economical means to help ensure your kids are covered as cyclists can often cover multiple dependents at the same time. As soon as your kid ages out of this protection, it may be possible to convert the rider into a brand-new plan.

When contrasting term versus long-term life insurance coverage, it is necessary to keep in mind there are a couple of different types. The most common sort of irreversible life insurance policy is whole life insurance, but it has some key distinctions contrasted to level term insurance coverage. Right here's a basic overview of what to take into consideration when comparing term vs.

Whole life insurance coverage lasts forever, while term protection lasts for a specific duration. The premiums for term life insurance policy are commonly less than whole life coverage. With both, the costs continue to be the very same for the duration of the policy. Entire life insurance policy has a money worth part, where a portion of the premium might grow tax-deferred for future requirements.

What should I know before getting Level Term Life Insurance Vs Whole Life?

One of the main functions of degree term coverage is that your costs and your fatality advantage do not transform. With reducing term life insurance policy, your costs stay the very same; nonetheless, the survivor benefit quantity gets smaller with time. You may have coverage that starts with a fatality benefit of $10,000, which can cover a home mortgage, and after that each year, the death advantage will reduce by a set quantity or percentage.

Due to this, it's typically an extra affordable type of level term coverage., yet it might not be sufficient life insurance coverage for your needs.

After making a decision on a plan, complete the application. For the underwriting procedure, you may need to supply general individual, wellness, way of life and work information. Your insurance company will certainly determine if you are insurable and the risk you may offer to them, which is reflected in your premium costs. If you're accepted, sign the documents and pay your very first costs.

You may desire to update your recipient info if you have actually had any type of considerable life modifications, such as a marital relationship, birth or divorce. Life insurance can occasionally really feel difficult.

What is a simple explanation of Level Term Life Insurance Protection?

No, level term life insurance coverage does not have cash worth. Some life insurance policy plans have a financial investment attribute that permits you to develop cash worth gradually. Guaranteed level term life insurance. A portion of your premium payments is reserved and can earn passion in time, which grows tax-deferred during the life of your insurance coverage

These policies are typically significantly more expensive than term coverage. If you get to completion of your policy and are still alive, the insurance coverage finishes. You have some options if you still desire some life insurance policy protection. You can: If you're 65 and your protection has actually gone out, for instance, you may want to buy a brand-new 10-year level term life insurance policy policy.

Is Level Term Life Insurance Protection worth it?

You may be able to transform your term insurance coverage right into a whole life policy that will last for the rest of your life. Several kinds of degree term policies are convertible. That means, at the end of your insurance coverage, you can convert some or all of your plan to entire life coverage.

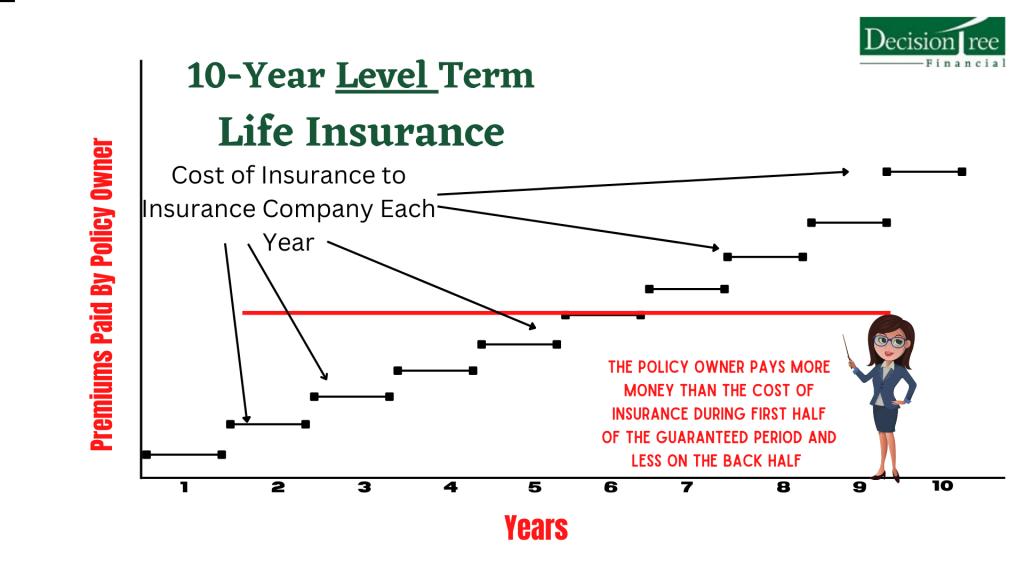

Degree term life insurance policy is a plan that lasts a collection term normally between 10 and 30 years and includes a level survivor benefit and degree costs that remain the very same for the entire time the plan is in impact. This implies you'll know precisely just how much your settlements are and when you'll need to make them, enabling you to budget plan accordingly.

Level term can be a fantastic alternative if you're seeking to buy life insurance policy protection for the very first time. According to LIMRA's 2023 Insurance coverage Barometer Research, 30% of all adults in the U.S. need life insurance policy and do not have any kind of kind of plan yet. Level term life is foreseeable and inexpensive, which makes it among the most prominent types of life insurance coverage

A 30-year-old man with a similar profile can anticipate to pay $29 monthly for the exact same protection. AgeGender$250,000 coverage amount$500,000 coverage amount$1 million coverage amount20Female$15$23$34Male$19$29$4830Female$15$23$37Male$18$29$4940Female$22$35$61Male$25$43$7550Female$44$78$139Male$57$102$18860Female$108$194$355Male$149$268$500 Collapse table Approach: Average month-to-month prices are determined for male and women non-smokers in a Preferred health category obtaining a 20-year $250,000, $500,000, or $1,000,000 term life insurance policy plan.

What is the difference between Level Term Life Insurance Premiums and other options?

Rates may vary by insurance company, term, protection quantity, health and wellness class, and state. Not all policies are available in all states. Price picture legitimate as of 09/01/2024. It's the most inexpensive kind of life insurance policy for most individuals. Level term life is a lot more cost effective than a similar whole life insurance policy policy. It's easy to take care of.

It permits you to budget plan and strategy for the future. You can conveniently factor your life insurance right into your spending plan because the costs never transform. You can prepare for the future just as quickly due to the fact that you understand precisely just how much cash your liked ones will get in case of your lack.

Level Term Life Insurance For Young Adults

In these instances, you'll typically have to go with a brand-new application process to get a much better price. If you still need protection by the time your level term life plan nears the expiry date, you have a few choices.

{kind=link}

Table of Contents

- – Why is What Is Level Term Life Insurance? impo...

- – What should I know before getting Level Term L...

- – What is a simple explanation of Level Term Li...

- – Is Level Term Life Insurance Protection worth...

- – What is the difference between Level Term Li...

- – Level Term Life Insurance For Young Adults

Latest Posts

Selling Final Expense Insurance

Instant Coverage Term Life Insurance

Instant Quote For Life Insurance

More

Latest Posts

Selling Final Expense Insurance

Instant Coverage Term Life Insurance

Instant Quote For Life Insurance